I think most bankers, being numbers people by trade, have some familiarity with the phrase in this headline, which is often associated with Mark Twain. At times, it has been suggested that your correspondent, a certified public accountant, can take numbers and analyses to a different (and possibly lower) level than the average financial professional. For the next four minutes, I am going to attempt to weave some observations about the current posture of community bank bond portfolios into a cogent column.

Spoiler alert: What follows is mostly positive commentary. As I have stated before, I hold portfolio managers in high regard. There are years of data that demonstrate how bankers can identify opportunities and, just as importantly, looming risks, and then adjust on the fly. Which is not to say they collectively act compulsively — it’s clear that community bankers have a highly developed sense of risk/reward dynamics.

Where We’ve Been

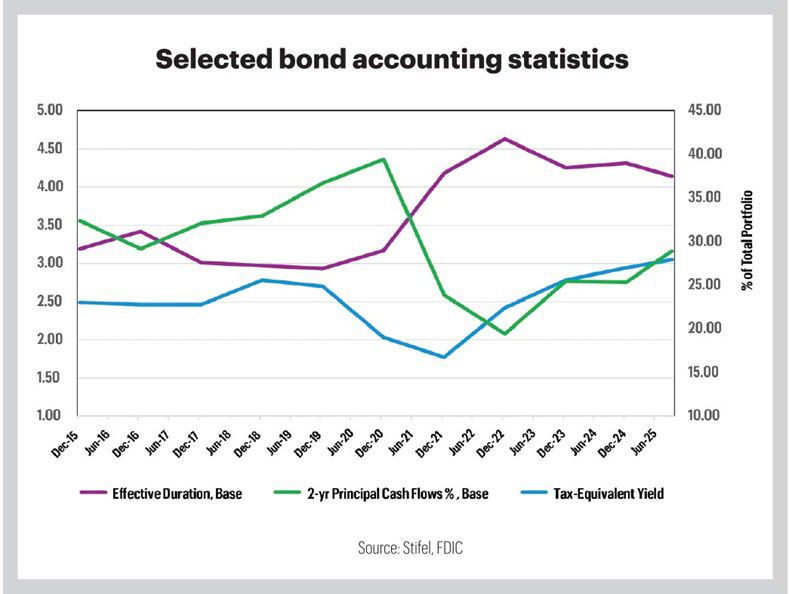

The previous table displays some key bond portfolio statistics going back a decade. Our data comes from the bond accounting population of ICBA Securities’ endorsed broker-dealer, Stifel. For a refresher, let’s recall where the community banking industry stood in 2015. It’s a good point to pick up this conversation, as it signaled a new phase in the Fed’s monetary policy. The FOMC raised the target level of fed funds from 0.25% to 0.50% in December 2015, marking the first change since the onset of the Great Recession in 2008.

The table reveals several residuals of that long stretch of low market yields. To wit: short durations, high levels of short-term principal cash flow and tax-equivalent yields that were not, shall we say, ambitious. Interestingly, yields didn’t really get any better until 2018, even though the Fed hiked overnight rates nine times in that three-year window. As low market rates endured for an extended period in the “teens,” average book prices consistently hovered in the 102 range.

What’s Happening Now

For the past three years or so, a different set of variables has emerged. The most durable (and cringe-inducing) metric is the unrealized loss. As of Sept. 30, the average portfolio had a loss of 7% or more. Since we’re finally embarking on a rate-cut cycle, those numbers should improve (shrink), though that’s largely dependent on how the long end of the yield curve reacts. Two positive and notable developments are the continued improvement in yields, which are now over 3% for the first time in at least a decade, and the normalization of the 24-month principal cash flows to the longer-term run rate of around 25% of the total bond portfolio. Effective durations are still longer than most community banks’ preferences but have declined since 2022, reflecting another positive trend.

What Else We’ve Seen

The “higher for longer” rate cycle has produced a couple of other benefits. The average portfolio’s book value is effectively par (100.00), which hasn’t been the case since before the Great Recession, around 18 years ago. This means that rate shocks, should they occur, won’t have a profound effect on book yields, since neither discount accretion nor premium amortization will be significant.

From the same chapter: The collection of bonds on hand can actually appreciate several percentage points before hitting the premium compression wall. If a group of bonds is owned at, say, 102 cents on the dollar, a drop in market yields will pull up the prices far less than if they’re owned at 100 cents on the dollar. So, the desirable element of convexity could come into play this year.

There is your update on the Xs and Os of well-built bond portfolios. It’s quite evident that ICBA members’ balance sheets are managed with care and thought. Portfolios are larger than they’ve ever been, but there’s no yield grab, and bankers have been patient with the unrealized losses, which continue to decline.

I’d like to wend back to the estimable Mr. Twain for a closing thought: “Substitute ‘damn’ every time you’re inclined to write ‘very’; your editor will delete it, and the writing will be just as it should be.” Or not.

Thank you to ICBA affiliates for your 2025 support!

ICBA Securities and its exclusive broker-dealer, Stifel, participated in education events for 29 ICBA state affiliates in 2025, marking the third consecutive year we’ve broken our own record for association event participation. We are grateful for the relationships we’ve made and look forward to more collaboration ahead.

Jim Reber, CPA, CFA (jreber@icbasecurities.com), is president and CEO of ICBA Securities, ICBA’s institutional, fixed-income broker-dealer for community banks.